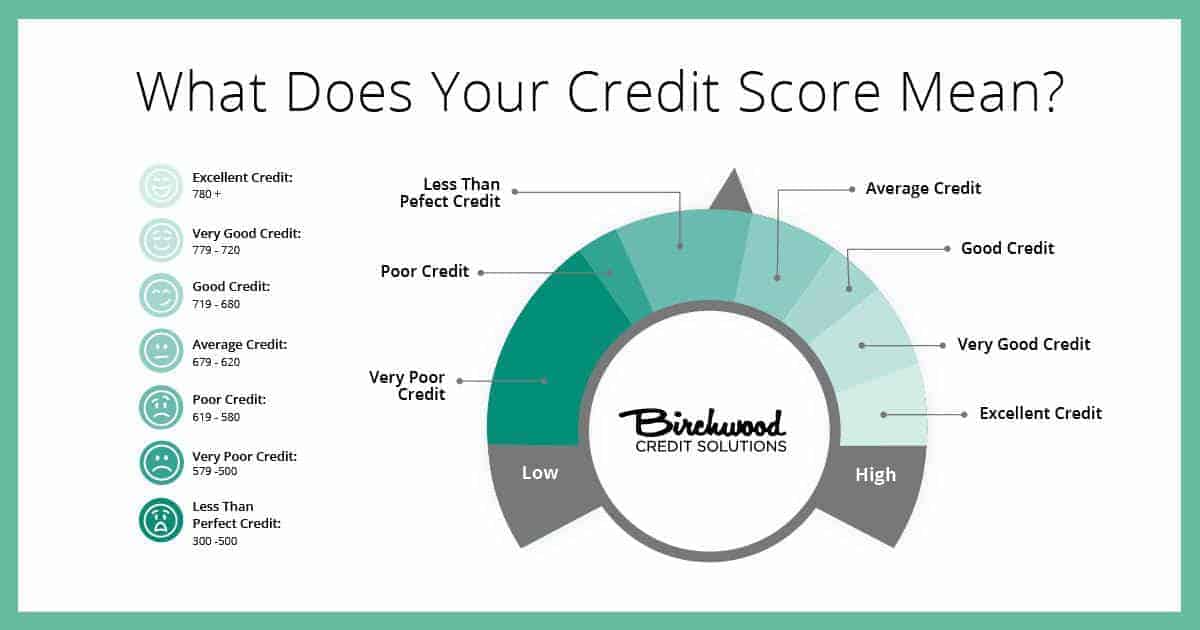

A credit score is a numeric valuation that lenders use, along with your credit report, to evaluate the risk of offering you a loan or providing credit to you. The FICO score is the most commonly used of the credit scores. It is calculated using different pieces of data from your credit report, including:

- payment history: 35%

- amount of debt relative to credit limit (credit utilization): 30%

- length of credit history (the longer the better): 15%

- types of credit in use (having current installment loans and revolving lines like credit cards helps): 10%

- new credit/recent credit applications (a hard inquiry can ding your credit for several months): 10%

Your credit score affects your ability to qualify for different types of credit – such as car loans and mortgages – and the terms you’ll be offered. In general, the higher your credit score, the easier it is to qualify for credit and obtain favorable terms. Because a lot could be riding on your credit score, it pays to keep track of it and to work towards improving it, when necessary. You can get a free credit report from each of the three big credit agencies – Equifax, Experian and TransUnion – but they will charge a fee if you want to see your actual credit score. The good news: You may be able to get your score for free from your bank or credit card issuer; here’s how.

Changing Times

Barclaycard US and First Bankcard (the credit card end of First National Bank of Omaha) were the first to sign on (in 2013) when the program launched, and since then others have joined in, including Citibank, Chase, Discover, Digital Credit Union, the Pentagon Federal Credit Union, U.S. Bank and North Carolina’s State Employees’ Credit Union. Ally Financial began offering free credit scores to auto loan customers in 2015, and Bank of America subsequently made credit scores available to cardholders for free.

Getting Your Score

If your bank or credit card issuer offers free credit scores, you should be able to check your score either online by logging into your account, or by reviewing your monthly statement. If you’re not sure whether your bank provides access to free scores, or if you have trouble finding your score, contact customer service for assistance. There are other resources to see your credit score or credit report for free, as well. If you’re wondering whether you should pay to see your credit score, the answer is probably “no.”

In addition to free credit scores, some banks offer benefits designed to help you understand – and improve – your score. First National Bank, for example, gives you 24/7 online access to your FICO score and shows you which key score factors have affected your number. And Barclaycard US provides your credit score, plus up to two factors that affect it, a historical chart that tracks it and email alerts any time your credit score has changed.

It’s important to note that not all credit scores are created equal, and the various banks and credit card issuers may provide access to different scores. Soon after the launch of the FICO Score Open Access Program, credit bureau Experian introduced a similar program, which allows banks to share its VantageScore credit score with consumers.

Today, these two systems operate on the same 300 to 850 point scale, and each uses similar criteria to calculate the scores, but they weigh each item differently. With FICO, for example, your payment history represents 35% of your score; for VantageScore, it accounts for around 40%. The result: The two scores will generally differ, even for the same person, on the same day. That’s not necessarily a bad thing, but it’s something to be aware of so that you can make sure you are comparing apples to apples when tracking your scores.

The Bottom Line

Your credit score affects your ability to obtain credit, and the terms you’ll be offered. Up until recently, the credit score industry was fairly covert, and it was difficult (or expensive) for most people to get their hands on their score. Today, however, a growing number of banks and credit card issuers provide credit scores free of charge, which is hugely valuable for consumers trying to track and improve their credit health.