Everyone who’s ever borrowed money to buy a car or a house or applied for a credit card or any other personal loan has a credit file.

Because we love to borrow money, that means almost every adult Canadian has a credit file. More than 21 million of us have credit reports. And most of us have no idea what’s in them.

Are there mistakes? Have you been denied credit and don’t know why? Is someone trying to steal your identity? A simple check of your credit report will probably answer all those questions. And it’s free for the asking.

So what’s in a credit report?

You may be surprised by the amount of personal financial data in your credit report. It contains information about every loan you’ve taken out in the last six years — whether you regularly pay on time, how much you owe, what your credit limit is on each account and a list of authorized credit grantors who have accessed your file.

Each of the accounts includes a notation that includes a letter and a number. The letter “R” refers to a revolving debt, while the letter “I” stands for an instalment account. The numbers go from 0 (too new to rate) to 9 (bad debt or placed for collection or bankruptcy.) For a revolving account, an R1 rating is the notation to have. That means you pay your bills within 30 days, or “as agreed.”

Any company that’s thinking of granting you credit or providing you with a service that involves you receiving something before you pay for it (like phone service or a rental apartment) can get a copy of your credit report. Needless to say, they want to see lots of “Paid as agreed” notations in your file. And your credit report has a long history. Credit information (good and bad) remains on file for at least six years.

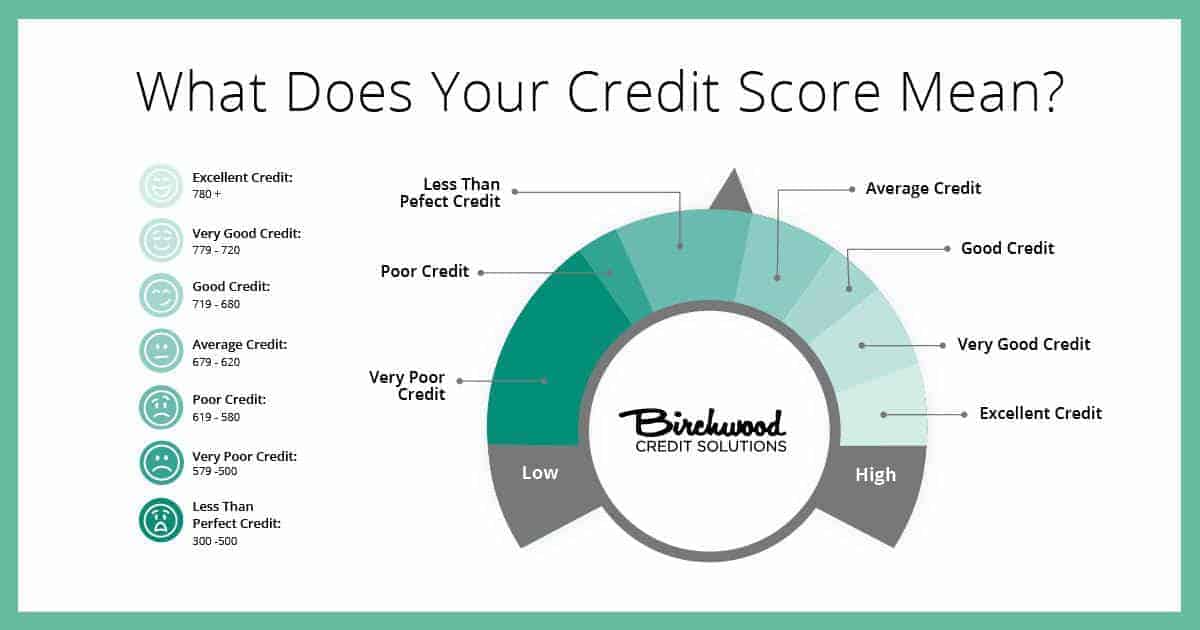

What’s a credit score? And why is it so important?

A credit rating or score (also called a Beacon or a FICO score) is not part of a regular credit report. Basically, it’s a mathematical formula that translates the data in the credit report into a three-digit number that lenders use to make credit decisions.

The numbers go from 300 to 900. The higher the number, the better. For example, a number of 750 to 799 is shared by 27 per cent of the population. Statistics show that only two per cent of the borrowers in this category will default on a loan or go bankrupt in the next two years. That means that anyone with this score is very likely to get that loan or mortgage they’ve applied for.

What are the cutoff points? TransUnion says someone with a credit score below 650 may have trouble receiving new credit. Some mortgage lenders will want to see a minimum score of 680 to get the best interest rate.

The exact formula bureaus use to calculate credit scores is secret. Paying bills on time is clearly the key factor. But because lenders don’t make any money off you if you pay your bills in full each month, people who carry a balance month-to-month (but who pay their minimum monthly balances on time) can be given a higher score than people who pay their amount due in full.

This isn’t too surprising when you realize that credit bureaus are primarily funded by banks, lenders, and businesses, not by consumers.

How can I get a copy of my credit report and credit score?

You can ask for a free copy of your credit file by mail. There are two national credit bureaus in Canada: Equifax Canada and TransUnion Canada. You should check with both bureaus.

Complete details on how to order credit reports are available online. Basically, you have to send in photocopies of two pieces of identification, along with some basic background information. The reports will come back in two to three weeks.

The “free-report-by-mail” links are not prominently displayed — the credit bureaus are anxious to sell you instant access to your report and credit score online.

For TransUnion, the instructions to get a free credit report by mail are available here. For Equifax, the instructions are here.

If you can’t wait for a free report by mail, you can always get an instant credit report online. TransUnion charges $14.95. Equifax’s rate is $15.50.

To get your all-important credit score, you’ll have to spend a bit more. Both Equifax and TransUnion offer consumers real-time online access to their credit score (your credit report is also included). Equifax charges $23.95, while TransUnion’s fee is $22.90. There is no free service to access your credit score.

You can always try asking the lender you’re trying to do business with, but they’re not supposed to give credit score information to you.