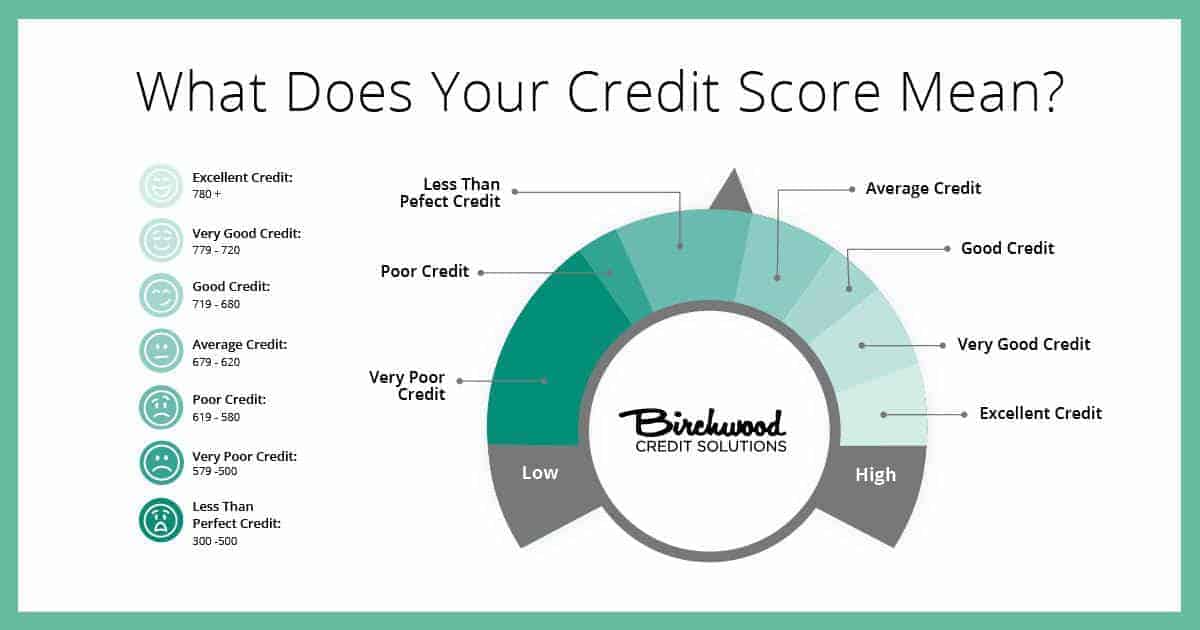

In Canada, credit scores range from 300 (just getting started) up to 900 points, which is the best score. According to TransUnion, 650 is the magic middle number – a score above 650 will likely qualify you for a standard loan while a score under 650 will likely bring difficulty in receiving new credit.

Lenders who pull your credit bureau file may see a slightly different number than you see when you pull your own file. This is due to the fact that each creditor applies a specific set of risk rules, giving and taking points for different purposes or preferences. This proprietary method of scoring will make a difference in the final calculation. The score you pull for yourself is calculated using an algorithm created for consumers that approximates these different formulas, and should still be in the same numerical range as the lenders’ scores.

Order your credit report from both credit reporting agencies in Canada – Equifax and TransUnion – at least once per year for free (when requested by mail, fax, telephone, or in person), and you can pay to see your credit score if you choose.

How can a low credit rating affect my life?

Credit scoring is used by lenders, insurers, landlords, employers, and utility companies to evaluate your credit behaviour and assess your creditworthiness.

1. Applying for a loan. Your credit score will be a big factor into the decision of whether you are approved or denied your application for more credit. Your credit score will also affect the interest rate and credit limit offered to you by the new credit grantor – the lower your credit score, the higher the interest rate will be and the lower the credit limit offered – the reason for this is you are considered more of a credit risk.

2. Applying for a job. A potential employer may ask your permission to check your credit file and based on what they read, they may decide not to hire you due to your poor credit history. Yes, having bad credit could cost you a job!

3. Renting a vehicle. When you sign an application to rent a car, the rental company can check your credit history to determine what their risk may be when they loan you their property. So although you are not applying for credit, the application documents you sign provide your written permission to access your credit information.

4. The same is true when applying for rental housing – the landlord may assess your tenant worthiness and their risk by factoring in your credit rating and score, and they could pass you over for someone with a better credit rating.

What information is used to calculate my credit score, and what factors will lower my score?

If you have tried looking on the consumer reporting agencies’ (CRAs, also know as Credit Bureaus) websites, you have seen they provide VERY little information as to how your credit score is calculated. They believe this information is proprietary and therefore their “secret”. They do, however, provide a list of the main factors which affect your credit score:

1. Payment History

Equifax says: “Pay all of your bills on time. Paying late, or having your account sent to a collection agency has a negative impact on your credit score.”

TransUnion says: “A good record of on-time payments will help boost your credit score.”

2. Delinquencies

Equifax lists: “Serious delinquency; Serious delinquency, and public record or collection field; Time since delinquency is too recent or unknown; Level of delinquency on accounts is too high; Number of accounts with delinquency is too high”

TransUnion lists: “Severity and frequency of derogatory credit information such as bankruptcies, charge-offs, and collections”

3. Balance-to-Limit Ratio

Equifax says: “Try not to run your balances up to your credit limit. Keeping your account balances below 75% of your available credit may also help your score.”

TransUnion says: “Balances above 50 percent of your credit limits will harm your credit. Aim for balances under 30 percent.”

Ok, so avoid maxing out your credit – because if you don’t really need more credit you’ll be able to get it, and if you do really need it then you are more of a risk.(Funny how that works)

4. Recent Inquiries

Equifax says: “Avoid applying for credit unless you have a genuine need for a new account. Too many inquiries in a short period of time can sometimes be interpreted as a sign that you are opening numerous credit accounts due to financial difficulties, or overextending yourself by taking on more debt than you can actually repay. A flurry of inquiries will prompt most lenders to ask you why.”

TransUnion says: “Avoid excessive inquiries. When a lender or business checks your credit, it causes a hard inquiry to your credit file. Apply for new credit in moderation.”