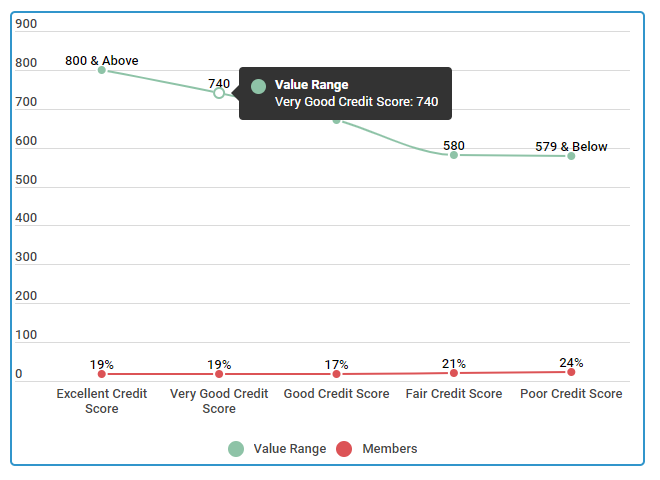

The most widely used credit score model FICO, ranges from 300 to 850. Consumers who fall between 720 and 850 typically qualify for the lowest interest rates or best credit cards. However, it’s important to understand there are a large number of different models used by lenders. Many of these use different scales, so a credit score of 650 can differ depending on the context.

Credit Score Ranges

There exist tens, if not hundreds, of different credit score models. Most consumers tend to focus on FICO 8, because it is most widely used by today’s lenders. However, not all credit-scoring models are equal. Some are better than others at predicting the creditworthiness of a particular individual, given a specific purpose. Large institutions will often purchase multiple models and use one when they deem it most appropriate.

| Credit Score | Range/Scale |

|---|---|

| Generic FICO Score | 300 – 850 |

| Equifax | 280 – 850 |

| TransRisk | 300 – 850 |

| VantageScore 1.0 & 2.0 | 501 – 990 |

| VantageScore 3.0 | 300 – 850 |

| PLUS Score | 330 – 830 |

| Experian National Equivalency Score | 360 – 840 |

One fact remains true in all the consumer scores listed above: higher scores are better than lower ones. Generally, people with a solid financial standing will have a score above 700 across all of these models. Most of the time, you will not have to do anything special for one credit scale versus another. Though certain factors are weighed differently from one model versus another, the same behavior will result in a good score. Make sure all of your payments are on time and that you maintain good standing across all of your loan/credit accounts. Over time, this type of behavior will ensure you fall into the best credit score ranges, no matter the model.

How Do Lenders Decide Which Credit Score Scale to Use?

A lender will opt to use a particular credit score model based on their preference and type of transaction being considered. Consider the example of a mortgage lender. Some may use VantageScore 3.0 because it penalizes late mortgage payments more than any other tardy bill. FICO, on the other hand, treats all late payments equally. The underwriters in the sample mortgage company may think this distinction is important enough to use one model versus another. You should also never assume a lender will always use the newest version of a score. Large financial institutions with a lot of legacy systems in place may use an older version of FICO for years due to legacy systems in place.

FICO tends to be the most forthcoming about the different industries that rely on its many models. For example, mortgage companies will typically use FICO® Score 2, 4 and 5 in evaluating their decisions. You can read more about the different FICO model versions on the company’s website.

How Do the Different Credit Score Ranges Compare to Each Other?

Fortunately, the Consumer Financial Protection Bureau (CFPB) found the different models were pretty similar in assessing credit worthiness. If you have an excellent FICO 8 score, chances are your VantageScore, TransUnion Risk score and others are fine as well. Therefore, it’s not necessary to seek out your personal rating across a wide array of credit score ranges.

| Correlation | Vantage vs. FICO Scale |

|---|---|

| Overall | 0.90 |

| Correlation for Customers Below Median | 0.77 |

| Correlation For Customers Above Median | 0.52 |

| Source: 2012 Consumer Financial Protection Bureau Study |

Correlation is expressed on a scale of -1.0 to +1.0. A negative correlation would imply two factors are inversely related. That is, while one is high the other is low. Statistically, a correlations above 0.5 implies a strong relationship between the two.

Consumers can use the CFPB’s approach to approximate the range they fall into based on knowing just one of their scores. The Bureau reduced consumer scores down to a relative one, based on their percentile. If you fall into the 70th percentile of FICO 8 users, you can estimate your range on another model by looking at where the 70th percentile lies on that scale. The table below shows the distribution of FICO 8 in the United States.

| FICO Score Range | Percent of Population |

|---|---|

| 300 – 499 | 4.9 |

| 500 – 549 | 7.6 |

| 550 – 599 | 9.4 |

| 600 – 649 | 10.3 |

| 650 – 699 | 14.0 |

| 700 – 749 | 16.6 |

| 750 – 799 | 18.2 |

| 800 – 850 | 19.9 |

Those who don’t want to guess can always take advantage of the multitude of services that provide credit scores to users. Many of these companies will generically refer to the number they show you as a ‘credit score’. You may have to call up the company or do a little bit of research to figure out what exact model they use. We expand more on this point in the following section.